If you’ve seen my previous article, you’d know that I have been taking points from Graham’s very prominent book titled “Security Analysis”. Once again let me reemphasize, whatever that will be stated is 100% from the text of Ben Graham and David Dodd Security Analysis and the purpose of this post is to serve as a reminder and summary of this very particular book. In this article, I will focus mainly on bond investing. Please be noted that whatever stated is base on the American market and therefore, some of the financial jargons may be unfamiliar to some of you.

- On bond investing, the key to success lies in avoiding losers, not in searching for winners

- We are confronted in many cases by a sudden disappearance of earning power, and a disconcerting question as to whether the business can survive

- “Buy and Hold” investing is inconsistent with the responsibilities of the professional investor, and the creditworthiness of every issuer represented in the portfolio must be revised no less than quarterly

- Don’t engage in market timing based on interest rate forecasts. Instead, we confine our efforts to “knowing the knowable”, which can result only from superior efforts to understand industries, companies and securities

- The investor must make certain by quantitative tests that the income has been amply above the interest charges and that the current value of the business is well in excess of its debts

- Safety is measured not by specific lien or other contractual rights, but by the ability of the issuer to meet all of its obligations

- This ability should be measured under conditions of depression rather than prosperity

- Deficient safety cannot be compensated for by an abnormally high coupon rate

- The selection of all bonds for investment should be subjected to the rules of exclusion and to specific quantitative tests corresponding to those prescribed by statute to govern investments of savings banks

- Regarding the shrinkage of values, companies should establish the practice of stating the original cost or appraised value of the pledged property as an inducement to purchase bonds is entirely misleading

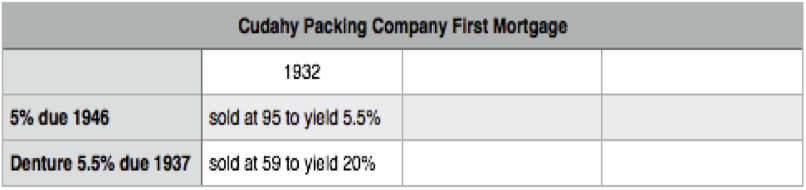

- Over-paying E.g.: The purchase of the 5% bonds at close to par could only be justified by a confident belief that the company would remain solvent and reasonably prosperous, for otherwise the bonds would undoubtedly suffer a severe drop in market price.

- But if the investor has confidence in the future of Cadahy, why should he not buy the debenture issue and obtain an enormously greater return on his money? The only answer can be that the investor wants the superior protection of the first mortgage in the event his judgment proves incorrect and the company falls into difficulties. It is clear that the investor who favors the Cudahy first-lien 5% is paying a premium of about 15% per annum (the difference in yield).

- On bond collapses, the public utility defaults were caused not by disappearance of earnings but by the inability of overextended debt structures to withstand a relatively moderate setback Pg 157

- The investor must not be to accept the issues of less desirable enterprises in the absence of better ones, but rather to refrain from any purchases on an investment basis if the suitable ones are not available. It appears to be a financial axiom that whenever there is money to invest, it is invested and if the owner cannot find a good security yielding a fair return, he will invariably buy a poor one

- Acknowledged risks of losing principal should not be offset merely by a high coupon rate, but can be accepted only in return for a corresponding opportunity for enhancement of principal e.g., through the purchase of bonds at a substantial discount from par or possibly by obtaining an unusually attractive conversion privilege

- Requirements for bond investments:

- The nature and location of the business or government

- The size of the enterprise

- The terms of the issue

- The record of solvency and dividend payments

- The relations of earnings to interest requirements

- The relation of the value of the property to the funded debt

- The relation of stock capitalization to the funded debt

- The values behind real estate mortgages are going-concern values: they are derived fundamentally from the earning power of the property. In other words, the value of the pledged asset is not something distinct from the success of the enterprise (as is possibly the case with a railroad equipment trust certificate) but is rather identical therewith

- Debt based on excessive construction costs: A sharp drop in construction costs would reduce fundamental values to a figure below the amount of the loan P.g 186

- From the authors’ viewpoint, an industrial preferred stock should be regarded as speculative unless combined charges and dividend requirements are earned at least twice over a period of years

- The real point is that where a company has both bonds and preferred stock the preferred stock can be safe enough only if the bonds are much safer than necessary Pg. 195

- The regular use of the face value of bond issues, rather than the market price, is recommended because it is much more convenient and does not involve the objections

- Stock value ratio for bonds: (3,150,000+13,900,000+128,200,000) / 10,500,000 = 13.8: 1

- Stock value ratio for 1st pfd: (13,900,000+128,200,000) / (10,500,000+3,150,000) = 10.4: 1

- Stock value ratio for 2d pfd: 128,200,000 / (10,500,000+3,150,000) 13,900,000) = 4.6: 1

- Interest on income or adjustment bonds is not part of the total interest charges when calculating the coverage for the fixed-interest bonds Pg. 206 (Margin of safety for income bonds)

- Instead of first computing the amount available for the charges, we divide the charges (and preferred dividends) into the balance after charges and add 1 to the quotient. Pg. 225 (Liability analysis)

- A subsidiary bond should not be purchased on the basis of the showing of its parent company, unless the latter has assumed direct responsibility for the bond in question

- Tendency of securities of insolvent companies to sell below their fair value:

- The company’s securities were selling together for less than one-third of the cash alone, and for only one-seventh of the net current assets, allowing nothing for the fixed property

- Failure to make a sinking-fund payment is regularly characterized in the indenture as an event of default, which will permit the trustee to declare the principal due and thus bring about receivership

- If a decline in profits should reduce the coverage to four times, he might prefer to switch into some other issue that is earning its interest eight to ten times

- The investor should not be stampeded into selling out holding with a strong past record because of a current decline in earnings

- “I’ll give you no numbers. I’ll give you no prices. I am not going to tell you which ones are going to succeed or fail. I think they are all pretty good companies, and if you bought a package of these stocks over the next three to four years, you would do very well… I hear this stuff all the time about how it is a bubble, it’s ridiculous. If you just use the numbers to do this stuff, number one, you won’t buy them, which is probably a good thing for some people. But you will never understand the amount of change that’s going on, and how much is still ahead of us.”

- Buying companies at 60% of intrinsic value or less

- The idea is to find valuable assets or inherently profitable companies that have nonetheless leveraged themselves up to levels of debt unsustainable by their cash flows

- A great investment opportunity occurs when a marvelous business encounters a one time huge but solvable problem

- Warren Buffet has often bought debt for a rate of return rather than for the creation of equity and obtaining of control

- A privileged senior issue, selling close to or above face value, must meet the requirements either of a straight fixed-value investment or of a straight common-stock speculation, and it must be bought with one or the other qualification clearly in view

- The investor interested in safety of principal should not abate his requirements in return for a conversion privilege Pg. 295 (Examples of an unattractive issue)

- Three important elements of profit-sharing privilege:

- The extent of the profit-sharing or speculative interest per dollar of investment

- The closeness of the privilege to a realizable profit at the time of purchase

- The duration of the privilege

- Even in the case of a convertible issue a callable feature is technically a serious drawback because it may operate to reduce the duration of the privilege

- The value of a common stock is said to be diluted if there is an increase in the number of shares without a corresponding increase in assets and earning power

- Unlike the case of a bond convertible into a preferred stock, there is usually a reduction in the coupon rate when a short-term note is converted into a long-term bond. The reason is that short-term notes are ordinarily issued when interest rates, either in general or for the specific company, are regarded as abnormally high, so that the company is unwilling to incur a steep a rate for a long-term bond