After such a long period, the topic on the cause of The Great Depression has yet to reach a definite answer. The Marxists contended that the depression was unavoidable under free-market capitalism as there was no restrictions on accumulations of capital which when over-accumulate will tend to lead to a crisis. On the other hand, Keynes argued that it was lower aggregate expenditures in the economy that contributed to massive decline in income and employment. In this article we will examine the cause of the Great Depression from the stand point of Monetarist, Milton Friedman.

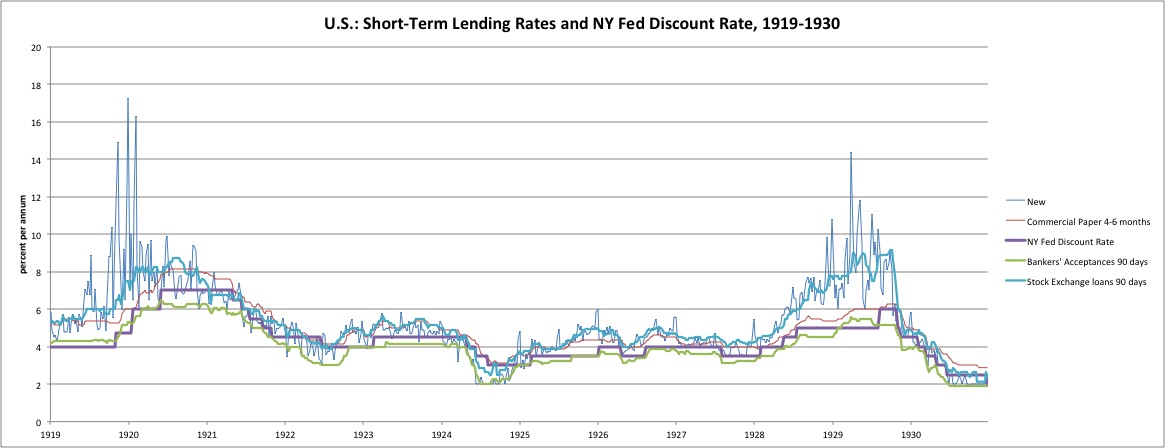

In his book titled A Monetary History of the United States 1867-1960, Milton Friedman and Anna Schwartz concluded that the Great Depression was not directly caused by the stock-market crash of October 1929. In the early 20s, the low interest rate prompted many investors to borrow from the banks, which led to speculation among investors and banks that slowly led to higher asset prices. At that point in time, the Fed was able to ease the depression had it raised interest rates to deflate soaring asset prices (bubble) that could potentially harm the economy.

Or better yet, after the stock market crash, the Federal Reserve allowed some large public banks to fail, which produced panic and widespread runs on other local banks while it sit idly by. The stock market crash changed the whole atmosphere within which businessmen were making their plans, and spread uncertainty, which reduced the willingness of both consumers and business enterprises to spend. Such effects were presumably accompanied by a corresponding effect on the balance sheets away from stocks to bonds, away from securities of all kinds toward money holdings. During the two months from August 1929 to the crash, production, wholesale prices and personal income fell at annual rates of 20%, 7.5% and 5% respectively. In the next twelve months, all three series fell at 27%, 13.5% and 17% respectively. The trend of the money supply changed from horizontal to mildly downward.

Had the Fed provided emergency lending (as thought to be its sole purpose when it was established in 1914) or conduct extensive open market operations to provide liquidity and increase the money supply, the rest of the banks would not have fallen after the large ones did. Throughout the period of 1929 – 1933, there were a total of three banking crisis coupled with Britain leaving the gold standard prolonged the depression. The problem with bank runs is that when depositors withdraw money and hold onto it rather than trust it to banks, it lowers the deposit-currency ratio; shrinking the money supply. Since banks operate through fractional-reserve banking, the economy experiences a multiple contraction of deposits. On top of that, the abandonment of gold standard by the Great Britain caused speculation that the United States would soon follow which led to a huge withdrawal of foreign deposits and gold outflow. Six weeks after 28th October 1931, the gold stock plunged 15% ($727 million).

The other explanation though uncommon was that the death of Governor Benjamin Strong Jr. caused monetary policy to change significantly. Strong’s understanding and application of monetary policy has helped alleviate recessions in 1924 and 1927 through aggressive open market operations and discount rate reductions. Sadly, his death produced a sharply different policy during the Depression.

The Great Depression from 1929 to 1933 was by far the most severe business-cycle contraction in the U.S. history. It was perhaps the most severe contraction worldwide, which saw net national product fell by more than one-half from 1929 to 1933 while stock of money falling by over a third. As such, it is often used, as a case study to analyze the root cause of recessions, thus, there is more than an answer to the cause of the depression. What I’ve provided are just the tip of an iceberg. To dig further on the root cause of the Great Depression from a monetarist’s point of view, I highly recommend reading “A Monetary History of the Unite States, 1867-1960” by Milton Friedman and Anna Schwartz.

Monetary policy should insure that there is sufficient money and credit available to conduct the business of the nation and to finance not only the seasonal increases in demand but the annual or normal increase in volume I believe that it should be the policy of the Federal Reserve System, by the employment of the various means at its command, to maintain the volume of credit and currency in this country at such a level so that, to the extent that the volume has any influence upon prices, it cannot possibly become the means for either promoting speculative advances in prices, or of a depression of prices – Governor Benjamin Strong Jr.